Finance

How to Choose the Best Car Insurance Policy in 2026

Buying car insurance used to feel simple. You paid the premium, kept the paper in the glovebox, and hoped you would never need it. In 2026, it is not that simple anymore. Prices can change from one insurer to another for the same car. Policy wording matters more than many drivers realize. Online comparison tools make it faster to buy, but they also make it easier to rush into the wrong choice. That is why choosing the best car insurance policy today is less about finding the lowest price and more about knowing what you are actually paying for.

For drivers in Saudi Arabia, this matters even more because insurance is not optional. At a minimum, third-party motor insurance is required, and the market now gives drivers several ways to compare, buy, renew, and manage policies online. Saudi rules also set out unified policy standards for compulsory motor insurance, while comprehensive cover works differently and can include deductibles, repair rules, add-ons, and claim settlement timelines that deserve close attention. Official platforms and insurers have also made car insurance Saudi Arabia online far easier to access, which is good for speed, but it also means one careless click can leave you underinsured.

This guide will walk you through how to choose the right policy in 2026, what to compare before you buy, how online car insurance Saudi Arabia works, which details most people miss, and how to avoid paying for a policy that looks good on paper but creates problems when you need to file a claim.

Why Choosing the Right Car Insurance Policy Matters More in 2026

The idea of “good insurance” has changed. A few years ago, many people judged a policy by one thing only: price. That habit still exists, but it does not work well in 2026. Two policies may look similar at checkout, yet one may give you approved workshop repairs, stronger claims support, clearer add-ons, and better protection against common risks like theft, flood, or major damage. The other may simply meet the minimum requirement and leave you with more out-of-pocket cost than you expected.

This is why the best car insurance policy is not always the cheapest one. It is the policy that fits your car, your budget, your driving habits, and your financial risk. If you drive a newer car, finance a vehicle, use your car daily for long distances, or park in busy areas, the wrong policy can become very expensive after one accident. If you own an older car with a lower market value, paying extra for features you may never use might not make sense either.

In Saudi Arabia, this decision also sits within a regulated structure. The unified compulsory motor insurance policy sets minimum third-party liability coverage standards, and insurers cannot agree to lower liability limits than those set in the policy. Comprehensive coverage goes beyond that, covering loss or damage to the insured vehicle and third-party civil liability, but the details can vary in important ways, especially in deductibles, repair channels, optional add-ons, and exclusions.

Another reason this matters more now is the growth of digital buying. Platforms in Saudi Arabia allow drivers to compare quotes and buy policies in minutes, which is convenient, but speed often pushes people to focus on the premium rather than the full value of the policy. Tameeni, for example, presents itself as an Insurance Authority-authorized platform for comparing and buying car insurance online from multiple providers, which shows how mature the online market has become. That convenience is useful, but it makes careful reading even more important.

What “Best” Really Means in Car Insurance

When people search for the best car insurance policy, they often mean different things.

Some want the lowest premium. Some want the fastest claims process. Some want the broadest protection. Some simply want a legal policy they can buy quickly online. These are not the same goal, and that is where buyers get confused.

The right way to think about “best” is this: the best policy is the one that gives you the right level of protection at a price you can comfortably afford, with conditions you fully understand.

The Cheapest Policy Is Not Always the Best

Low premiums can be attractive, especially when you are renewing and just want to get it done. But a cheaper premium may come with a higher deductible, fewer repair options, stricter exclusions, limited add-ons, or weaker service after an accident. If the policy only looks good before a claim, it is not really a good policy.

For example, comprehensive policy rules in Saudi Arabia allow a deductible amount stated in the policy schedule for each claim involving damage to the insured vehicle, and the insurer’s liability starts only after that deductible is exhausted. That means the amount you pay upfront after an accident matters. A low annual premium with a high deductible can cost you more overall if you actually need to use the policy.

The Most Expensive Policy Is Not Automatically the Best Either

Some drivers overbuy because they assume a higher premium must mean better protection. That is not always true. You may be paying for extras that do not fit your car or your real risk level. A practical driver with an older vehicle may not need every add-on available. A driver with a brand-new financed vehicle may need broader protection and dealership repair access. Context matters.

“Best” Depends on the Driver Profile

A new driver will judge value differently than an experienced driver with a clean claim history. Someone with a family SUV has different needs than a person using a compact sedan for city travel. A vehicle parked outdoors every day carries a different exposure than one kept in a secured garage. A person who wants a fully digital service may value online account tools and claim tracking more than someone who prefers branch support.

This is why a blog about the best car insurance policy should not push one blanket answer. It should help the reader choose well.

What’s New With: Why Shipping Insurance Is Essential

Understanding the Main Types of Car Insurance in Saudi Arabia

Before comparing insurers, you need to understand what you are comparing.

Third-Party Liability Insurance

Third-party insurance is the minimum legal requirement for drivers in Saudi Arabia. The unified compulsory motor insurance policy sets the minimum civil liability coverage against third parties, and insurers cannot set liability limits below the official standard. In simple terms, this policy protects you against liability for damage or injury caused to others, but it does not generally protect your own car from damage in the same way comprehensive insurance does.

For many drivers, third-party cover is the budget option. It may suit an older vehicle with low market value, where paying for full comprehensive coverage no longer makes economic sense. But it also means you carry more personal risk if your own vehicle is damaged.

When Third-Party Insurance Makes Sense

Third-party insurance may be suitable if your car is old, has a low resale value, or would cost more to insure comprehensively than the likely benefit you would receive. It may also work for drivers who use the vehicle infrequently and want only the legal minimum.

When Third-Party Insurance May Not Be Enough

If you rely on your car daily, own a newer or financed vehicle, or would struggle to pay for repairs or replacement after a major accident, third-party cover may leave you exposed. It can be the cheapest policy today and the most expensive mistake tomorrow.

Comprehensive Car Insurance

Comprehensive insurance gives broader protection. Under Saudi rules for comprehensive motor insurance, coverage includes loss or damage to the insured vehicle and third-party civil liability. The policy can cover damage from incidents including fire, theft, lightning, and natural disasters such as floods or hailstones, subject to policy conditions.

This is often the better choice for newer vehicles, higher-value cars, leased or financed vehicles, and drivers who want stronger financial protection.

What Comprehensive Insurance Usually Covers

Comprehensive cover generally protects the insured vehicle itself, not just the damage you cause to others. It may also include options around repair at approved workshops or dealerships, towing expense limits under certain conditions, and additional covers offered before policy issuance, such as roadside assistance, rental replacement, accidents outside the Kingdom, or personal accident and medical expense cover for the insured or named driver.

What Comprehensive Insurance Does Not Automatically Cover

Many drivers assume “comprehensive” means “everything.” It does not. Exclusions still apply. Saudi rules list exclusions such as driving without a valid license matching the vehicle type, racing or speed testing, driving under the influence of drugs, alcohol, or medically prohibitive medicine, overload in cases where that caused the accident, and use of the vehicle as working machinery, among others.

That is why reading exclusions matters just as much as reading benefits.

How to Choose Between Third-Party and Comprehensive Cover

The choice is not simply about price. It is about your ability to absorb loss.

If your car is worth a significant amount and you cannot easily replace or repair it out of pocket, comprehensive insurance is often the safer route. If your car is older and you would likely replace it rather than repair it after major damage, third-party insurance may be enough.

A simple way to think about it is this: ask yourself what would happen if your car were badly damaged tomorrow. If the answer is that the repair or replacement would create real financial stress, paying more for broader coverage can be the smarter decision.

Questions to Ask Yourself Before Choosing the Cover Type

How much is my car worth today?

A car’s current market value matters more than what you paid for it. Insurance should be tied to realistic value, not your emotional attachment to the vehicle.

Could I afford a large repair bill this month?

If the answer is no, comprehensive cover deserves serious attention.

Is the car financed or leased?

Many financed or leased arrangements require stronger coverage because another party has a financial interest in the car.

How often do I drive?

High mileage generally means greater exposure to risk.

Where do I drive and park?

Busy roads, crowded parking, and outdoor parking can all increase risk.

The Core Factors to Compare Before Buying Any Policy

A smart buyer does not compare insurers only by premium. The better method is to compare the total policy value.

Premium Cost

Yes, price matters. But it should be the starting point, not the final decision. Compare the premium alongside the deductible, repair options, claim support, exclusions, and add-ons. A lower premium can hide higher costs later.

Deductible Amount

For comprehensive policies, the deductible is what you pay before the insurer starts covering damage to your own vehicle. In Saudi Arabia, the deductible is stated in the policy schedule, and the insurer’s liability begins after it is exhausted for insured vehicle damage claims.

A higher deductible can reduce the premium, but it also means more out-of-pocket expenses when a claim happens.

Repair Method and Workshop Access

This is one of the most overlooked parts of choosing the best car insurance policy. Some policies may direct repairs through approved workshops. Others may include dealership repairs or allow specific repair channels, depending on what is stated in the policy schedule. Saudi comprehensive rules note that if a claim is accepted as partial loss, the insurer shall approve repair at the respective certified dealership or certified auto repair shops approved by the insurer, as specified in the policy schedule.

If you care about original parts, dealership repair history, or brand-standard service, this point is too important to skip.

What’s New With: Cost Savings Through Insurance Legacy System Transformation

Claim Settlement Timelines

Good insurance should not only pay. It should pay in a reasonable time. Under Saudi comprehensive motor insurance rules, the insurer must acknowledge receipt of the claim and inform the claimant of any missing documents within 3 business days. If the claim is accepted as partial loss, the insurer shall approve repairs within 5 business days. If the loss is total, settlement should take place within a maximum of 10 business days from the date the claim file is completed with all required documents.

These rules matter because they help you judge what service standard to expect.

Add-On Coverage

Optional extras may include roadside assistance, replacement car rental, personal accident cover, medical expenses for the insured or named driver, accident cover outside the Kingdom, and coverage for related drivers or domestic workers in certain policy structures. These add-ons can change the real value of a policy.

Exclusions

Always read exclusions with care. Many claim disputes start because the buyer never looked at this section. If you know what is excluded, you will choose with clearer eyes.

How Online Buying Has Changed Car Insurance in Saudi Arabia

The rise of car insurance Saudi Arabia online has changed the way people shop. Instead of visiting branches or speaking to several companies one by one, drivers can now compare, buy, and receive policies digitally.

Platforms like Tameeni present insurance offers from multiple providers and describe their service as a fair comparison platform that helps users compare prices and product information from service providers so users can make a decision and follow up. Tameeni also says users can compare third-party car insurance prices online, pay, and receive a policy in minutes, and its site states it is authorized by the Insurance Authority.

This digital shift has made online car insurance Saudi Arabia much more practical for everyday drivers.

Benefits of Buying Car Insurance Online

Buying online saves time, makes quote comparison easier, and allows drivers to review options at their own pace. It can also help you see differences between insurers more clearly than a rushed sales call would.

For many drivers, online buying creates a better research process because the information is in front of them. They can compare price, provider, and often policy elements in one place.

The Risk of Buying Too Fast

The downside is speed. Many people treat online insurance like booking a delivery app order. They pick the lowest figure and move on. That approach can work only if all policies are identical, and they are not.

A smarter online buyer slows down at the final step. Before paying, check the deductible, workshop access, exclusions, add-ons, and claims process. Convenience is helpful, but only when it does not replace judgment.

Step-by-Step Process to Choose the Best Car Insurance Policy in 2026

Now let’s turn all this into a practical selection process.

Step 1: Know Your Car’s Real Risk Profile

Start with the vehicle itself. Note its age, current market value, mileage, usage pattern, and where it is parked most of the time. A two-year-old SUV used every day in city traffic has a very different risk profile from a ten-year-old sedan used twice a week.

Step 2: Decide Your Coverage Goal

Ask whether you want legal minimum protection or broader protection. This single choice narrows the market fast. If you already know third-party is not enough for your situation, there is no value in comparing it against comprehensive policies as if they solve the same problem.

Step 3: Compare Multiple Quotes

Do not judge one quote in isolation. Comparison matters because pricing models differ by insurer, driver profile, and car profile. This is where car insurance Saudi Arabia online becomes useful. Online comparison tools can save time and help you see the market more clearly.

Step 4: Read the Policy Summary, Not Just the Price

Once you have a shortlist, stop looking at premium for a moment. Read the essential coverage features. Check the deductible, repairs, add-ons, and exclusions.

Step 5: Check the Claims Path

The real value of a policy shows after an accident. In Saudi Arabia, Najm provides online accident reporting and post-accident e-services, and the official site describes its service as a free service to complete post-accident procedures. That is useful, but your insurer’s own claim handling still matters.

Step 6: Review Exclusions Line by Line

Do not skip this. It is the part most people regret ignoring.

Step 7: Check Whether You Qualify for Discounts

Saudi rules and past official announcements have included no-claims discounts on motor insurance. SAMA’s 2017 announcement stated a discount of 15% of the new basic price for one year without claims, increasing to 30% for three years without claims. Some comprehensive products may also offer no-claims or loyalty-related pricing features depending on the policy structure and underwriting rules.

Even if the discount framework varies across products or providers, a clean claims history can be financially valuable.

Step 8: Buy Only After Checking the Final Schedule

The policy schedule matters. That is where many important details live: insured amount, deductible, repair basis, covered drivers where relevant, and other terms.

Common Mistakes People Make When Choosing Car Insurance

A detailed article about the best car insurance policy would be incomplete without the mistakes section, because avoiding bad decisions is often more useful than chasing perfect ones.

Buying Only on Price

This is the biggest mistake. A low premium can hide weak value.

Ignoring the Deductible

People often notice the deductible only after the claim happens. By then it is too late.

Assuming Comprehensive Means Everything Is Covered

It does not. Exclusions still apply, and they can be serious.

Not Checking Workshop Terms

Repair quality and location matter more than people think.

Forgetting About Natural Disaster or Theft Exposure

Saudi comprehensive rules explicitly note coverage scope can include fire, theft, lightning, floods, and hailstones under policy conditions. That is a major value point for drivers in risk-prone situations.

Not Understanding the Claims Procedure

An accident is stressful. If you do not know what to do next, the process feels worse.

What to Know About Claims in Saudi Arabia Before You Buy

A policy is only as good as its claim experience.

In Saudi Arabia, Najm plays a central role in accident reporting and post-accident support. The official Najm site offers online accident reporting and e-services and describes itself as handling post-accident procedures, including claim-related steps.

For comprehensive claims, Saudi rules also give important timelines. The insurer should acknowledge the claim within 3 business days and notify you of missing documents. Accepted partial-loss claims should move to repair approval within 5 business days, while completed total-loss claims should be settled within a maximum of 10 business days. If theft occurs, the insured must promptly report it to the authorities and the insurer, and the claim is accepted only after 60 days from the report date.

These timelines do not remove every delay, but they do give you a useful benchmark for what fair handling should look like.

Why Claims Knowledge Helps You Choose Better

When you understand the claims path before buying, you make a sharper choice. You stop thinking like a shopper and start thinking like a future claimant. That mindset helps you focus on what really matters.

How No-Claim History Can Affect Your Choice

If you have a clean driving and claims history, do not treat it as a small detail. It can help reduce costs over time.

Saudi official guidance from SAMA in 2017 stated that the no-claims discount reaches 15% of the new basic price for one year without claims and rises with the number of years without claims, reaching 30% for three years without claims. The rulebook for certain comprehensive leasing-related products also mentions no-claims and loyalty discounts under the underwriting instructions.

This matters in two ways. First, it can reduce your premium. Second, it means frequent small claims may not always be worth filing, depending on the damage amount, your deductible, and the long-term premium effect. That is not a reason to avoid valid claims. It is simply part of making a financially smart choice.

How to Find the Best Policy if You Want to Buy Online

Many readers searching for online car insurance in Saudi Arabia want the fastest path without making a weak decision. Here is the practical approach.

Compare First, Do Not Buy First

Use online tools to gather options, not to rush into checkout. Compare multiple insurers side by side.

Verify the Platform

Use authorized and credible providers. Tameeni’s site states that it is authorized by the Insurance Authority and offers a comparison of multiple insurance providers. That kind of authorization claim matters because insurance buying involves regulated financial products.

Read the Provider Information Carefully

The comparison platform may help you shop, but the policy itself still comes from an insurer. Pay attention to the actual insurer behind the offer.

Save the Policy Documents Immediately

Keep the policy wording, schedule, payment record, and any claim contact details.

Final Thoughts

Choosing the best car insurance policy in 2026 is really about making a calm, informed decision before you are forced into a stressful one after an accident. Good insurance should match your real risk, protect your finances, and make the claims process easier, not more confusing. In Saudi Arabia, drivers have the advantage of a regulated motor insurance structure, official claims support through Najm, and growing access to online car insurance Saudi Arabia comparison tools that make shopping easier than before. But easy access should not lead to careless buying.

If you remember one thing, remember this: the right policy is not the one with the lowest price on the screen. It is the one you will still be glad you bought on the day you actually need it.

A car insurance quote can feel random until you look under the hood.One driver gets a price that seems fair. Another gets a much higher number for what looks like the same car. Then a third driver changes one detail, like the deductible or type of cover, and the quote shifts again. That is the moment many people stop and ask the real question: how are Car Insurance Premiums actually calculated?

The short answer is that insurers do not pull prices out of thin air. They study risk, expected claim cost, repair exposure, policy terms, and the details you give them. In Saudi Arabia, that process is not meant to be casual. Official Saudi rules say insurers must collect full exposure data to finalize a motor quotation, must use book rates unless claims experience is credible enough to do otherwise, and cannot give one flat third-party price for all vehicles because quotes must be vehicle-type dependent at a minimum.

That matters because many drivers think price is just about the car. It is not. The car matters, but so do the coverage type, insured value, deductible, optional covers, and the insurer’s view of expected losses. Saudi rules on comprehensive motor insurance also tie pricing back to the sum insured, deductible, and optional coverage listed in the policy schedule. For leased vehicles, the rules state that the premium is calculated annually based on changes in the sum insured and pricing factors for the lessee.

This article explains the subject in plain language. It breaks down what Car Insurance Premiums are, what steps insurers use to calculate them, why quotes differ so much, and what drivers should know when comparing car insurance quotes in Saudi Arabia. If you have ever looked at a policy price and felt lost, this guide is built to make the logic clear.

What Car Insurance Premiums Really Mean

A premium is the price you pay for insurance cover. That is the simple definition, but it helps to go one step further. A premium is the amount the insurer charges to take on a defined set of risks for a defined period under a defined contract.

That last part matters. You are not paying for a vague promise. You are paying for a specific level of protection with specific limits and specific conditions. When the insurer calculates Car Insurance Premiums, it is trying to estimate how much risk it is taking on, how much claims may cost, and what it needs to charge to cover that exposure under the policy terms. Saudi underwriting rules state that no insurer should provide a quotation without adequate underwriting information, including claims experience, to determine premium rates scientifically for the policy terms and conditions offered.

That is why the same driver can see very different prices for third-party and comprehensive cover. The insurer is not just selling “insurance.” It is pricing a contract. A policy that only covers third-party liability is a very different risk from a policy that also covers your own car, theft, fire, natural disaster damage, towing, and optional extras. Saudi comprehensive motor rules define the insured vehicle’s sum insured, deductible, and optional coverage limits as core parts of the policy schedule, which shows how closely price follows policy structure.

When people compare car insurance Saudi Arabia quotes, they often look only at the final number. That is a mistake. The number is the result of many moving parts. If you only compare price and ignore the coverage behind it, you are not really comparing policies. You are comparing labels.

The Basic Logic Behind How Car Insurance Premiums Are Calculated

At a simple level, insurers start with a base rate and then adjust it based on risk. That is the easiest way to understand the process. The base rate reflects the insurer’s starting price for a category of risk. The adjustments come from the details of the vehicle, the driver, the claims background, the coverage chosen, and the policy conditions.

Saudi rules support this broad pricing logic. The quotation instructions require insurers to determine book rates for motor quotations unless claims experience is fully credible, and they must determine experience or burning cost rates when enough claims history exists. The same rules also say that third-party quotations must be vehicle-type dependent at a minimum and cannot be one flat price for all vehicles.

The Base Rate

The base rate is the insurer’s starting point. It is built from actuarial and underwriting work. That includes the insurer’s historical claims costs, exposure patterns, repair trends, and policy structure. Saudi underwriting rules say motor pricing reports should be updated to take recent claims experience into account, which shows that base pricing is expected to reflect real loss experience, not guesswork.

This means the quote is rooted in data. Even before your personal details are applied, the insurer already has a view on how risky a class of vehicle or policy type tends to be. That is why two categories of cars often start from different price levels before anything else changes.

Vehicle Risk

The vehicle itself shapes the quote in a big way. Saudi rules do not allow third-party pricing to be flat across all vehicles, which confirms that insurers must treat vehicle type as a real pricing factor.

Why does vehicle type matter so much? Because vehicles differ in repair cost, part prices, claim severity, accident patterns, and total loss exposure. A small sedan, a high-value SUV, and a performance car do not create the same financial risk for an insurer. If repairs are expensive or the insured value is high, the insurer has more money at risk. That usually pushes the premium up.

For comprehensive policies, the insured value matters even more. Saudi comprehensive rules define the sum insured as the value of the motor vehicle stated in the policy schedule, and policy coverage limits for damage or loss to the motor vehicle are tied to that sum insured.

Claims Experience and Expected Losses

A strong part of motor pricing is claims experience. Saudi underwriting rules are clear on this point. Insurers must obtain claims experience and enough underwriting data to finalize quotations, and they must use experience or burning cost rates when the number of vehicles or amount of experience is sufficient under the actuary’s threshold.

In plain language, this means past losses matter. If a risk has a history of claims, that history can affect the premium because it changes the insurer’s view of future cost. Claims experience does not guarantee that another claim will happen, but it does influence how the insurer prices the chance and likely cost of future losses.

This is one reason Car Insurance Premiums are not static. They are not based on one idea alone. They respond to what the insurer has learned from real claims data.

Policy Terms and Conditions

The quote also depends on what the policy promises to cover and how it handles loss. Saudi underwriting guidance specifically mentions that quotations must reflect the policy terms and conditions offered.

That matters because two policies can look similar in marketing and still be different in cost. One may offer a broader repair route. Another may include more helpful optional covers. One may have a lower deductible. Another may have a higher insured value. Small contract differences can change the expected cost to the insurer, which changes the premium.

What’s New With: Jamar Champ Net Worth: Business Ventures, Growth, and Financial Legacy

The Main Factors That Affect Car Insurance Premiums

Once the basic pricing structure is in place, the insurer applies the details that make the quote yours. This is the part most drivers care about because it is where the premium begins to move up or down in a visible way.

The Type of Coverage You Choose

This is one of the strongest pricing factors. Third-party liability cover and comprehensive cover do not price the same because they do not cover the same risk.

Saudi Arabia’s unified compulsory motor insurance policy is built around civil liability toward third parties and sets minimum liability terms and limits for that cover. Saudi comprehensive motor insurance rules go further and cover damage or loss to the insured vehicle, with minimum scope that includes fire, theft, natural disaster damage such as floods and hail, plus towing and storage, subject to the policy terms.

That difference matters. If the insurer is only covering your liability to others, the exposure is narrower than if it is also covering your own car. So comprehensive cover usually costs more than basic third-party cover. That does not mean it is overpriced. It means the insurer is taking on a larger share of risk.

This point is especially important when comparing KSA car insurance quotes online. A lower number may simply mean lower protection. It does not automatically mean better value.

The Sum Insured or Vehicle Value

For comprehensive cover, the sum insured is a major part of the price. Saudi comprehensive rules define the sum insured as the vehicle’s value shown in the policy schedule, and the coverage limit for damage or loss to the vehicle follows that amount.

The logic here is simple. A car worth SAR 150,000 usually costs more to insure comprehensively than a car worth SAR 45,000 because the insurer may have to pay much more in a total loss or severe damage case. Higher value raises the possible payout. Higher possible payout usually raises the premium.

This is why Car Insurance Premiums often change over time even if your driving habits do not. As vehicle value changes, the pricing may change too. Saudi rules for comprehensive insurance of leased vehicles explicitly say the premium is calculated annually based on changes in the sum insured and pricing factors for the lessee.

Vehicle Type and Repair Exposure

Vehicle type does more than affect insured value. It also affects repair exposure. Even where two vehicles have similar market values, they may not cost the same to insure if one has costlier parts, more expensive labor needs, or higher claim severity.

Saudi quotation instructions require third-party pricing to be vehicle-type dependent at a minimum. That official rule alone tells you that vehicle class is not a minor detail. It is part of the pricing base.

This matters a lot in car insurance Saudi Arabia comparisons because some buyers assume make, model, or class only affect comprehensive policies. In practice, vehicle type matters even for compulsory third-party quoting.

Deductible or Excess

A deductible is the amount the insured pays before the insurer pays the rest on certain claims under comprehensive cover. Saudi comprehensive rules define the deductible, require it to be stated in the policy schedule, and clarify that the insurer’s liability for damage or loss to the motor vehicle begins after the deductible has been applied. The rules also say this does not apply to third-party civil liability claims.

The pricing effect is direct. A higher deductible often lowers the premium because you are agreeing to carry more of the smaller loss yourself. A lower deductible usually raises the premium because the insurer is taking on more of that cost.

This is one of the clearest trade-offs in motor insurance. Some people focus on lowering the premium and choose a high deductible without thinking about what that means at claim time. That can backfire. A cheaper policy can feel expensive later if the out-of-pocket amount is more than you are comfortable paying.

Optional Covers and Add-Ons

Optional covers can increase the premium because they increase the insurer’s obligation if a covered event happens. Saudi comprehensive motor rules require insurers, during negotiation and before issuing the policy, to offer optional covers such as replacement vehicle rent, roadside assistance, medical expenses or physical injury cover for the insured or named driver, and accidents occurring outside Saudi Arabia. The policy also allows optional coverage limits to be listed in the schedule.

Each add-on has a price effect because each add-on can create more possible claim cost. A policy with roadside assistance, replacement car benefit, and broader driver-related protection will not price the same as a stripped-down policy with none of those features.

That does not mean add-ons are bad. It means you should view them for what they are: extra cover with extra cost. Some are worth it. Some are not. The right answer depends on how you use your car and what kind of loss would hurt you most.

Claims History and Credibility of Experience

Claims history is central to pricing, especially where the risk has enough data behind it. Saudi quotation rules say insurers must determine experience or burning cost rates unless the number of vehicles is below the threshold set by the actuary. Saudi underwriting rules also state that actual rates cannot be provided without sufficient data divided by the rating factors used in the underwriting manual.

This shows that pricing is not only about broad assumptions. It can be shaped by real claims performance when enough experience exists. That principle is easy to understand. A risk with a heavier loss pattern usually costs more to insure than a risk with a lighter one.

Even if a driver does not see every calculation in the background, that logic still affects the price shown on the screen.

How Car Insurance Premiums Are Calculated in Saudi Arabia

Saudi pricing rules give useful clues about how the system works in practice. They do not hand out a simple public formula like “premium equals X plus Y minus Z.” Insurance does not work that way. But the official framework shows the building blocks insurers must use and the data they must collect.

Insurers Must Price With Real Underwriting Data

One of the clearest official points is that insurers need full underwriting information and claims experience before they can issue actual rates. Saudi underwriting guidance says a quotation can be given as an illustration based on the information provided, but the insurer must amend the quotation using full underwriting data and may not issue a policy on quoted rates until it has enough data for an accurate quotation.

That tells you something important about car insurance Saudi Arabia pricing. The quote is not just a website estimate floating in space. It is supposed to reflect real policy inputs. If the inputs change, the premium can change too.

What’s New With This Topic: Andrea Palmer TTI: Powering Global Legal Leadership

Book Rates Come First Unless Credible Experience Exists

Saudi quotation instructions say insurers must determine book rates for all motor quotations unless the amount of claims experience is sufficient to be fully credible. They also require experience or burning cost rates where enough experience exists.

In plain language, that means insurers start with structured rates and then use stronger claims data when they have enough of it. This is one reason KSA car insurance pricing may shift when the insurer has more accurate exposure or claims information than it had before.

Third-Party Insurance Cannot Be One Flat Price for All Vehicles

Saudi quotation rules state that any third-party liability quotation must be vehicle-type dependent at a minimum and that it is not permitted to quote a flat fixed cost for all vehicles covered.

That is a useful point for consumers because it explains why two third-party quotes can still differ a lot. Some drivers think only comprehensive pricing changes sharply by vehicle. The official rules show that even compulsory third-party pricing must reflect at least the vehicle type.

Comprehensive Premiums Reflect Sum Insured and Policy Structure

Saudi comprehensive rules define the sum insured, deductible, and optional coverage limits as part of the policy schedule. For leased vehicles, the rules say the premium is recalculated annually based on changes in the sum insured and pricing factors for the lessee.

That means comprehensive pricing is tied closely to the structure of the cover. If the insured value changes, if the deductible changes, or if the optional covers change, the premium can change too. That is not arbitrary. It follows the contract.

Why Two People Rarely Pay the Same Premium

This is where the topic becomes real for readers. People often compare their quote with a friend’s quote and feel annoyed when the numbers do not match. But insurance is not priced like a ticket with one standard entry fee. It is priced risk by risk.

One person may have a different vehicle class. Another may choose comprehensive instead of third-party. One may have a different deductible. Another may add roadside assistance and replacement vehicle rent. One quote may be based on different underwriting inputs or claims experience. Saudi rules support all of those pricing differences because the quote must reflect real exposure data, vehicle type, experience where credible, and the exact policy structure being offered.

That is why Car Insurance Premiums are personal even when the general method is systematic. The framework is organized, but the result changes with the details.

Why the Cheapest KSA Car Insurance Quote May Not Be the Best Value

A low premium feels good at first. That reaction is normal. But price without context can fool you.

A cheaper policy may come with a higher deductible. It may have a lower insured value. It may remove useful optional covers. It may limit the repair route in a way that affects your claim experience. It may simply be third-party cover while another quote is comprehensive. Saudi comprehensive rules make clear that repair handling, sum insured, deductible, and optional cover limits are all policy-level items that shape the protection you actually receive.

This is one of the most important ideas in KSA car insurance shopping. The right question is not, “Which quote is lowest?” The better question is, “What am I getting for this premium, and what would I have to pay myself after a loss?”

A policy that saves a little money now but leaves you with a large bill later is not really cheap. It only looked cheap on the purchase screen.

How to Read a Quote More Clearly

A car insurance quote becomes easier to judge when you stop treating it like a mystery number and start reading the parts behind it.

First, look at the coverage type. Is it only third-party liability, or is it comprehensive? Saudi compulsory motor insurance is designed around third-party civil liability, while comprehensive motor rules add protection for the insured vehicle and can include covered losses such as fire, theft, and natural disaster damage.

Next, look at the sum insured if the policy is comprehensive. This tells you the value the insurer is using for your vehicle. Then look at the deductible. That tells you what part of covered own-damage loss you may need to pay first. After that, review optional covers. If the quote includes roadside assistance, replacement car rent, or added driver protection, those benefits may be affecting the premium. Saudi rules explicitly list such options as covers insurers must offer during the negotiation stage before issuing the policy.

Reading a quote this way does more than help you compare price. It helps you compare actual protection.

Smart Ways to Lower Car Insurance Premiums Without Weakening the Policy Too Much

There is no magic trick that makes Car Insurance Premiums drop while everything else stays perfect. Price and protection always affect each other. Still, there are sensible ways to improve value.

One option is to review the deductible. A higher deductible can lower the premium, but only choose a level you could comfortably pay after a claim. Saudi comprehensive rules make clear that the deductible is a real cost that applies to damage or loss to the insured vehicle.

Another step is to review optional covers honestly. Some extras are useful. Some may not fit your needs. Since optional benefits such as replacement vehicle rent and roadside assistance can add to the premium, removing an add-on you do not need may reduce cost while keeping the core cover strong.

It also helps to compare like with like. A fair comparison means the same coverage type, same insured value, same deductible, and similar options. Without that, one quote may look cheaper simply because it covers less.

For drivers checking car insurance Saudi Arabia, the best savings often come from a cleaner comparison, not from chasing the lowest number without reading the details.

Common Myths About How Car Insurance Premiums Work

One common myth is that insurers simply charge whatever they want. That is not how regulated motor pricing is supposed to work in Saudi Arabia. Official rules require underwriting information, book rates, credible claims experience where available, and vehicle-type dependent third-party pricing.

Another myth is that comprehensive pricing is just inflated third-party pricing. That is wrong because comprehensive cover takes on more risk. Saudi rules for comprehensive motor insurance include the insured vehicle’s loss or damage and can include fire, theft, natural disaster damage, towing, storage, and optional extras, all of which can affect expected claim cost.

A third myth is that the lowest premium always means the smartest choice. That only sounds true when you ignore deductible, repair terms, insured value, and policy scope. Once you look at the contract, the cheapest number may stop looking attractive.

Final Thoughts

So, how are Car Insurance Premiums calculated?

They are built from risk, not luck. Insurers start with structured rates, apply underwriting data, look at claims experience when credible, and price the policy according to vehicle type, insured value, deductible, policy terms, and optional covers. In Saudi Arabia, the official framework makes that clear. Third-party pricing cannot be a flat price for every vehicle. Insurers must collect enough data to issue actual rates. Comprehensive pricing is tied closely to the sum insured and the structure of the policy schedule.

That is the big takeaway for anyone comparing car insurance Saudi Arabia policies or trying to understand a KSA car insurance quote. The premium is not just a bill. It is the price of a specific level of risk transfer. When the risk is broader, the price is usually higher. When the contract is narrower, the price may be lower. What matters is whether the policy matches your real exposure and whether you understand what the number includes.

A good insurance decision starts when the price stops being the only thing you look at.

The global market for gold and silver is one of the most watched. Every trading day, their prices are affected by a mix of geopolitical, economic and financial forces. These changes are closely monitored by traders, investors and consumers because precious metals’ price fluctuations can be a reflection of broader economic conditions or investor sentiment. Market participants can make better decisions if they are aware of the key factors that affect daily gold and silver prices. This article explores the key drivers of price fluctuations and why they can occur.

7 Factors That Influence Current Silver & Gold Prices Daily

1. Global Economic Indicators and Monetary Policy

The broader data on the economy and monetary policies are two of the biggest daily influences of gold and silver prices. The precious metals market is influenced by inflation, interest rate expectations, GDP growth, employment figures, and inflation reports.

Investors often turn to gold or silver when inflation is higher than anticipated as a hedge against currency erosion. Prices are usually driven up by this demand. When central banks signal rate reductions, such as the U.S. Federal Reserve, non-yielding metals like silver and gold become more attractive because the real returns are lower. In contrast, investors can be pushed lower by strong economic indicators and expectations of higher interest rates.

As traders react to new economic predictions, they may adjust their positions as a result of the Federal Reserve’s action and expectations.

2. U.S. dollar strength and currency movements

Currency fluctuations directly affect the daily movements of gold and silver prices, which are priced globally in U.S. Dollars. Gold and silver are more expensive when purchased in other currencies. This generally reduces demand, and pushes prices lower. A weaker dollar boosts prices and demand because it reduces the cost to foreign buyers.

The daily changes in the currency market — driven by macroeconomic data, trade statistics, or geopolitical events — can cause an immediate change in precious metals price.

3. Supply and Demand Fundamentals

The fundamentals of supply and demand also influence the daily price movement. Silver supply is constrained compared to gold, which has stockpiles above ground and a consistent production. This is because silver is a secondary product of mining base metals like zinc, copper and lead. Silver supply is less sensitive to increases in price, so tighter markets may emerge when demand grows.

Silver is a valuable metal that can be used in both industrial and investment applications. Silver demand from electronic, solar panel, electric vehicle (EV) and medical uses often adds to the upward pressure of prices. This is especially true during times of strong industrial activity.

4. Geopolitical events and Safe-Haven Flows

The geopolitical risks are a key factor in the daily movements of precious metal prices. Investors have historically used gold as a “safe-haven” asset during periods of financial or political instability. The price of silver can benefit as well from the safe-haven flow, but its volatility is higher due to its small market size and lack industrial demand.

Recent geopolitical tensions, tariff uncertainty and investor anxiety have led to sharp increases in gold and silver as they seek safety from the global turmoil.

5. Investment Flows and Market Liquidity

Investor behavior and the market’s sentiment are important factors in determining short-term prices. ETFs that own physical silver and gold can experience rapid flows of money based on the risk appetite of investors, which affects prices in near real-time. Gold or silver ETFs that are heavily bought tend to push prices up, while those with significant sales put downward pressure.

Futures and Options markets, where traders make predictions about future prices movements, can also increase short-term volatility. Price swings can be caused by large speculative position, margin calls or abrupt changes in the market’s sentiment.

6. Jewellery and Retail Demand

The jewelry market remains an important component in gold and silver consumption, especially on markets such as India and China. Retail purchases are often influenced by seasonal events such as weddings and festival seasons. This spike in demand for physical goods can affect the daily prices in local markets.

7. Technical and Seasonal Factors

Short-term prices can be affected by seasonal and technical trading patterns. Chart levels such as support and resistance are closely monitored by traders. They also pay attention to volume trends, moving averages and key chart lines. Prices can move when they approach certain technical levels. This is because automated buying or selling may occur. In the past, there have been recurring patterns of demand, including increased sales during holidays and lower trading volume on holidays. This can cause price fluctuations to be exaggerated.

Stay Updated with Current Silver & Gold Prices

To make smart investment or purchase decisions, tracking Current Silver & Gold Prices in real time is essential. Daily price updates reflect a dynamic interplay of global economic data, currency fluctuations, geopolitical developments, and industrial demand. By monitoring live pricing charts and up-to-date market analysis from reputable sources like SilverGoldPrice.com, you can stay informed about market trends and react swiftly to changes that may affect your precious metals portfolio.

Conclusion

Prices of gold and silver fluctuate daily as a result of a variety factors, including economic data, expectations about interest rates, changes in currency, geopolitical situations, and global shifts in supply and demand. Silver’s industrial uses make it more volatile. While gold prices are largely driven by the fact that they act as safe haven assets, their role in a market is to be viewed as an asset of safety. These factors can help investors and buyers make better decisions and anticipate trends in a market that is constantly changing.

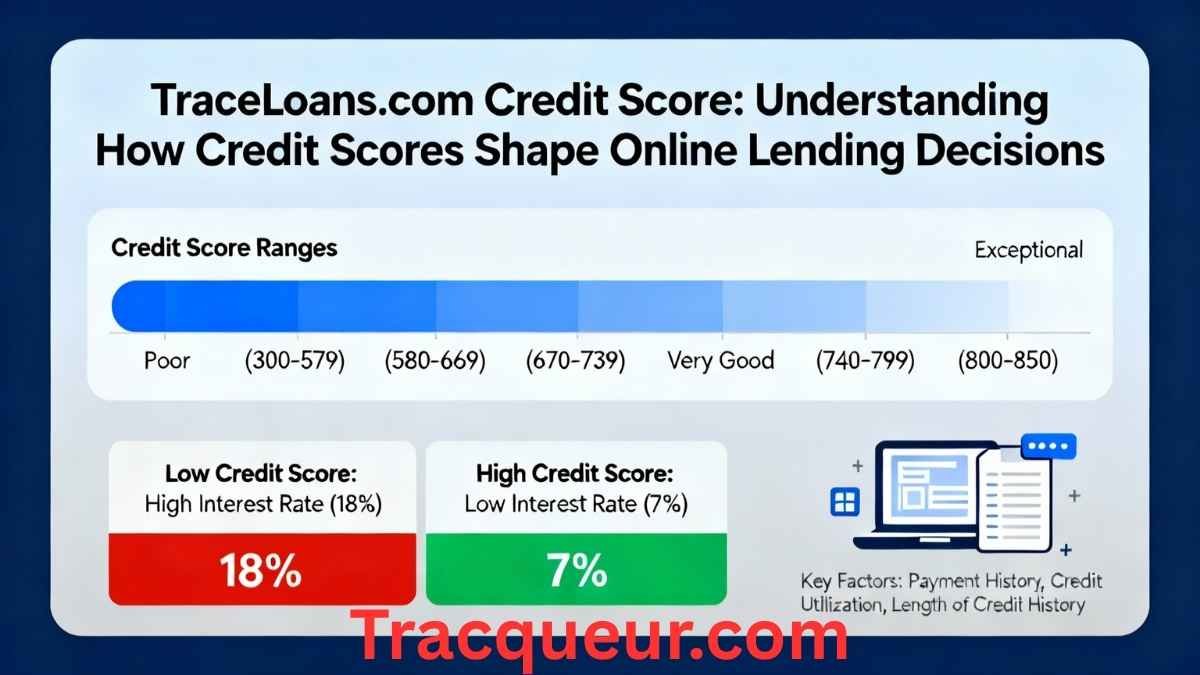

Introduction to TraceLoans.com and Credit Scores

TraceLoans.com credit score discussions usually come up when people start exploring online lending platforms and want to understand how creditworthiness affects loan eligibility. Credit scores play a central role in almost every modern lending decision, especially in digital-first financial services.

Online loan platforms like TraceLoans.com operate in a competitive environment where speed, automation, and risk assessment are crucial. Credit scores help lenders quickly evaluate an applicant’s financial behavior without lengthy manual reviews.

From an expert perspective, understanding how credit scores interact with platforms like TraceLoans.com empowers borrowers to make smarter decisions. It shifts the focus from confusion to clarity, especially for first-time or credit-conscious borrowers.

What a Credit Score Really Represents

A credit score is a numerical summary of an individual’s credit behavior. It reflects how responsibly someone has managed borrowing, repayments, and overall financial commitments over time.

Factors such as payment history, credit utilization, length of credit history, and recent inquiries all influence the score. Contrary to popular belief, income alone does not determine creditworthiness.

Experts emphasize that a credit score is not a judgment of character. It is a financial risk assessment tool used to predict the likelihood of repayment, especially in automated lending environments.

How Online Lending Platforms Use Credit Scores

Platforms like TraceLoans.com rely heavily on credit scores to streamline loan approvals. Automated systems analyze scores alongside other data points to assess risk efficiently.

A higher credit score typically signals lower risk, which may result in better loan terms, faster approvals, or higher borrowing limits. Lower scores may still qualify but often under stricter conditions.

From a technical standpoint, credit scoring allows online platforms to scale operations. Instead of manual underwriting, algorithms make consistent decisions based on established risk models.

TraceLoans.com Credit Score Requirements Explained

While specific requirements vary, TraceLoans.com credit score considerations generally align with industry standards. Applicants are usually evaluated within a credit score range that reflects acceptable risk levels.

Some borrowers assume that online lenders only cater to high-score applicants, but that is not always the case. Many platforms consider a broader spectrum, including fair or average credit profiles.

Experts advise borrowers to read eligibility criteria carefully. Understanding minimum expectations helps avoid unnecessary applications that could impact credit through repeated inquiries.

Credit Score Impact on Loan Approval and Terms

Credit scores do more than determine approval; they influence loan structure. Interest rates, repayment periods, and fees are often directly tied to score ranges.

A stronger credit score typically results in lower interest rates, reducing the overall cost of borrowing. This difference can be significant over the life of a loan.

From a financial planning perspective, improving credit before applying can lead to long-term savings. Even small score increases can result in better loan conditions.

Common Credit Score Misconceptions

One common misconception is that checking your own credit score lowers it. In reality, soft checks do not affect scores, while hard inquiries from loan applications may.

Another myth is that closing old accounts improves credit. In many cases, this can shorten credit history and negatively impact scores.

Experts stress the importance of accurate information. Misunderstanding credit behavior often leads to decisions that unintentionally harm financial health.

Improving Your Credit Score Before Applying

Improving a credit score does not happen overnight, but consistent habits make a difference. Paying bills on time remains the most impactful factor.

Reducing credit card balances and avoiding unnecessary new credit applications also help stabilize scores. Small adjustments can produce noticeable improvements over time.

From an expert standpoint, preparation matters. Borrowers who plan ahead often secure better outcomes when applying through platforms like TraceLoans.com.

Alternative Factors Beyond Credit Scores

While credit scores are important, many online platforms consider additional data. Income stability, employment history, and existing debt levels may also be evaluated.

Some platforms use alternative data models to assess borrowers with limited credit history. This approach helps expand access without compromising risk management.

Experts view this trend as a positive evolution. It recognizes that financial responsibility can exist beyond traditional credit scoring systems.

Responsible Borrowing and Financial Awareness

Understanding TraceLoans.com credit score requirements encourages responsible borrowing. Loans should be tools for growth, not sources of long-term financial strain.

Borrowers are advised to assess affordability before applying. Knowing repayment obligations helps prevent missed payments that could damage credit further.

From a financial literacy perspective, awareness leads to better decisions. Responsible borrowing supports both personal stability and long-term credit health.

Security and Data Protection Considerations

When applying online, borrowers often share sensitive financial data. Platforms like TraceLoans.com are expected to use secure systems to protect this information.

Encryption, verification processes, and secure data handling are essential for maintaining trust. Users should also take steps to protect their own devices and credentials.

Experts recommend caution and research. Understanding privacy policies and platform credibility is part of responsible financial engagement.

The Future of Credit Scoring and Online Lending

Credit scoring models are evolving. New technologies and data sources are shaping more inclusive and accurate assessments.

Online platforms will likely continue refining how they evaluate creditworthiness. This could lead to fairer access and more personalized loan offerings.

From an expert perspective, adaptability is key. Borrowers who stay informed about credit trends will benefit most from future lending innovations.

Final Thoughts on TraceLoans.com Credit Score

TraceLoans.com credit score discussions highlight the importance of understanding how modern lending works. Credit scores remain central, but they are part of a broader financial picture.

Borrowers who understand their credit position are better equipped to navigate online lending platforms confidently. Knowledge reduces uncertainty and improves outcomes.

Ultimately, credit scores are tools, not barriers. When approached with awareness and preparation, platforms like TraceLoans.com can support informed and responsible borrowing decisions.

How to Choose the Best Car Insurance Policy in 2026

How Car Insurance Premiums Are Calculated

Slot Gacor Kali Gbowin: The Rising Name in Online Gaming

Fakboitv: Exploring the Digital Identity Behind a Rising Online Brand

MoreSexyASMRGirls and the Evolution of Digital ASMR Culture